There has been a slightly more cautious start to the 22/23 tax year than in 21/22 from both the VCT fund managers, who are tending to bring offers a little bit later to the market, and from investors themselves who have been slightly slower to invest, with even the most popular VCTs taking a little bit longer to receive funds this year. However, barring yet another U-tum from the latest iteration of the UK government in the next few days, the sunset clause for VCTs, enterprise investment scheme (EIS) and seed enterprise investment scheme (SEIS) has been extended during the mini-budget, and the expectation from VCT market commentators is currently that we may see similar levels raised as last tax year, even with significant economic headwinds and volatility in the financial markets.

The recent history/ backdrop

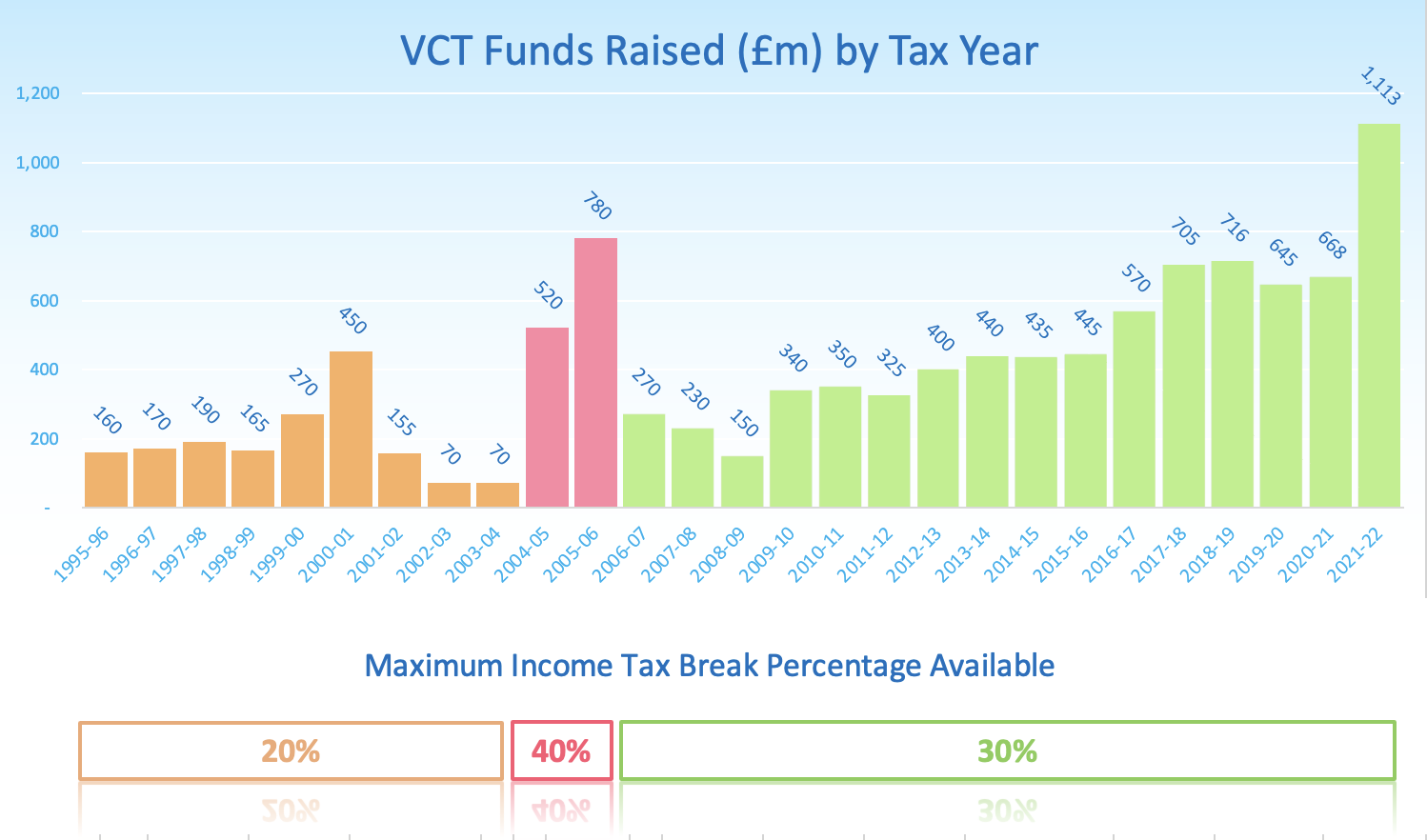

VCTs raised £1.13bn in the 2021/22 tax year. It is the highest amount of funds ever raised within a single tax year since their launch in 1995/96, and an increase of over 150% on the previous tax year, albeit that the previous years were inevitably slightly affected and dampened down by the COVID 19 global pandemic. However, the 2021/22 tax year raise should be seen in the context of the steady growth curve that we saw in advance of the pandemic As show in Fig 1 below (Source, HMRC).

The Story so far for the 22/23 Tax year

Last year saw an incredibly quick raise by Amati AIM in July and things picked up quite quickly from there, as previously explored in our articles of last year, there were technological contributing factors to that as well. This year, as at the end of October, VCT raise figures were trending c. 15% behind their position of 12 months ago, with a little over £225M raised this year. However, this is not necessarily representative of a loss of investor appetite for VCT investments, rather an indication that some of the most popular VCTs had not opened, or had not opened quite as early.

The Mobeus VCTs, now part of the Gresham House stable that also includes Baronsmead VCTs, have proved incredibly popular both last year tax year and this, and quickly raised £45M within 48 hours, a similar speed to last year, and are currently sitting at £70M with the Mobeus 2 & 4 already full.

Octopus AIM VCTs have already opened and closed full this year. With many of the popular names open and newcomers like Guinness and Edition Capital coming to the market we’re currently looking at an indicative raise level of over £700m with overallotment of a further £370 and some big names still to come.

So the VCT supply and investment opportunity appears to be out there, and investor appetite seems to be there for the most popular VCTs at least, though the speed of raises across several VCTS is slower than last year. The wider environment is certainly at play here, the Hargreave Hale AIM VCT has so far raised £23m in 65 days versus £40m in 50 days last year, and that would surprise no-one given the turbulence in the AIM markets, which are c.30% down on last year.

However this is not the full story why raises are taking longer, at least some of the reduction in speed is being put in deliberately by the VCT industry itself, so as to provide a bit more control around the client applications and client funds coming on board. As bank transfers and applications have moved predominantly online, the application form/data is naturally separate from the bank transfer (as opposed to the traditional cheque stapled to a paper form), and as such the Receiving Agent has quite a matching and reconciliation job to do based on references, quantity and client names.

When managed through a solution such as that offered by GrowthInvest, in which we typically hold client funds on platform, there is clear managed process and we work closely with receiving agents to ensure the funds and applications are matched and clarified. Unfortunately last tax year saw a significant number of applications that were never followed by the required investments, leading to some raises which had closed and initially appeared to have overfunded, being perilously close to not achieving their full raise amount.

This has led to a couple of slight changes coming into play: Firstly that many providers are publishing their prospectuses and accompanying documentation in advance of providing a final application form, on or off line. This allows advisers to speak to their clients, kick off with their suitability, and for industry analysts to get going on the production of their reports. It has also been reclarified that no applications should be made in advance of the official “open” – even if documents are available.

The second trend we are seeing is a much shorter time span between the application form being declared valid, and the required time for the client funds to be with the receiving agent and reconciled. For example with Mobeus, there was a 5 working day limit imposed. If funds had not arrived by this point, the client would effectively lose their place in the accepted applications, and risked being bumped out. A combination of our technical links with receiving agents, and our client services team keeping a close eye on proceedings, and liaising with all parties whenever required helps to dramatically reduce the chances of this happening.

The guests On our VCT Adviser Hour (available on demand) thought that the likely brake on the raise this year was going to be overall capacity rather than any lack of overall confidence.

AS Paddy Lamb, Associate Director at Foresight Group put it: “The upper limit of VCT fund raising is much more likely to be defined by lack of supply rather than lack of demand”. This sentiment was echoed by other guests including Matt Currie from Seneca Partners, and Harry Heartfield from Edition Capital. All noted that despite a view of growing demand for VCTS, the economic situation would clearly affect this year’s raise to some extent.

The Bigger Picture

GrowthInvest Head of Investments Steve Dobson feels that, despite the somewhat turbulent economic and political situation, the underlying attraction of building up a VCT portfolio remains strong for the right sort of investors:

“Alongside the attractive 30% initial income tax break, there are sound investment reasons for looking at earlier stage companies across a range of sectors, and a lot of very experienced managers providing the support and expertise that they need. For clients who have reached their LTA, a VCT portfolio offers a very attractive additional element to sit alongside pensions and ISAs, providing decent tax free dividends and the potential for really significant growth.

VCTs, along with EIS and SEIS investments should be looked upon as a long term investment. Markets work in cycles and we’ve just experienced a long bull market that even the COVID pandemic struggled to stifle. There are significant headwinds out there right now and people’s disposable income is being stretched with the cost of living crisis brought on in a large part by the supply chains being impacted by ongoing COVID implications and the war in Ukraine. It can seem hard to look beyond the day to day but in every downturn there is potential opportunity and whilst none of us have a crystal ball to see when markets and economies will recover, valuations are down across AIM and private companies providing VCT and EIS investors with lower entry points.

We have also been working with a number of adviser firms and their clients in helping to provide a bit of additional liquidity to existing established VCT portfolios, where we can offer a bespoke service to clients to find a market for existing VCTs beyond the 5 year holding period

The overall trend and attraction of VCTs remains strong and at the time of writing Octopus Titan has just come to market with its intention to raise £175m with an overallotment facility for a further £75m. Should Octopus be successful in raising the full £250m, this would demonstrate a 25% increase year on year on funds raised, coming from an already elevated base of £200m last year. With some other popular VCTs still to come such as Baronsmead, British Smaller Companies and Puma Alpha could we possibly see final raise levels somewhere near the record levels of last year?